3) B is such that for all firms f

Presentation for teachingpurposes of part of Cools, K., hamminga, B. and Kuipers, T. (1994) "Truth Approximation by Concretization in Capital Structure Theory" in: hamminga B. and N.B. de Marchi (eds) Idealization VI: Idealization in Economics. Poznan Studies in the Philosophy of Science and the Humanities, Vol 38. Amsterdam, Atlanta: Rodopi 205-28.

1 Interesting theorems

This section displays the logical skeleton of "A state-Preference Model of Optimal Financial Leverage" by Kraus and Litzenberger (1973).

As usual in theoretical economics, the strategy of model construction is focused on an interesting theorem (hamminga (1983)). Here, what is to be derived is a theorem on how the value of (debt plus equity of) a firm depends on the proportion of debt in that value.

Modigliani and Miller (1958)(1963) used a plausible model to arrive at implausible, and therefore intriguing theorems: the proportion of debt has no influence at all on the value of the firm if corporate tax is nonexistent, and should be 100% if corporate tax exists. The model of Kraus and Litzenberger based on a state preferance approach, could explain the existence of an optimal solution between 0% and 100%

2 State preference

The "state preference" approach consists of assuming a set J of all conceptually possible end- of- period "states of the world" j. In every single possible state of the world j there is a fixed and given return Xfj for every firm f, a given tax rate Tj and given bankruptcy cost Cfj (Cfj = 0 for firms f that survive in state j).

It is a one period analysis. The return (earnings before interest and taxes) Xfj of firm f in state j is identical to the end- of- period market value of firm f. If you would know what state j would be realized you would have no problems of uncertainty. Hence, the problem of uncertainty solely consists of investors not knowing what state will be realized, and having different probability beliefs concerning j � J.

A "market expectation" about the states j � J is negotiated among investors by assuming tradeable "primitive securities" Pj, which can be thought of as "lottery tickets" yielding 1$ if state j occurs and nothing if j` � j occurs. The equilibrium price Pj of Pj could be derived from 1) probability beliefs of investors concerning state j 2) their time preference for holding money, 3) their risk aversion and 4) their utility functions (Arrow (1969), Debreu (1959)). Kraus and Litzenberger do not perform this derivation, but take Pj, j � J as given, exogenous variables. Any other security bought by an investor can now be identified with a definite number of lottery tickets Pj for every state j (since investors are assumed to know the return of every security in every state).

3 Potential models (conceptual framework)

Now we are ready to specify wat structure a thing x should have in order to be a conceptual possibility in the language that Kraus and Litzenberger have chosen for their theory.

x is a potential debt equity market system with corporate tax and bankruptcy cost ("x is a DETCp") iff (if and only if)

x = < J,F,Y,R,P,D,X,T,C,P,Y,Z,B,S,V,>

The symbols J,F,Y,R, denote elementary sets. Their meanings are

J the set of states of the world j

F the set of firms f in the market system

Y

the set of primitive securitesR the set of real numbers

The symbols P,D,X,T,C,P,Y,Z,B,S,V denote functions:

P

: J � Y yields the primitive security Pj that has a return of 1 $ if state j occurs, and 0 $ in any state j` � j.D: F

� R+D yields the debt of firm f, a promise to pay a fixed amount Df, irrespective of the state that occurs, a nonnegative real numberX: F x J

� RX yields the return of f in state j, the end of period value of f, a real number Xfj, negative in case of bankruptcy.T: J

� RT[0,1] yields the tax rate over X in state j, a real number Tj in the closed interval [0,1].C: F x J

� R+C is the bankruptcy cost Cfj of f in state j, zero if the firm survives in state j.With the help of the primary functions

P,D,X,T,C, the secundary functions P,Y,Z,B,S,V, are defined.12)P:

Y � R+p yields the price Pj of primitive security PjY: F x J x R+D x RX x R+C

� R+Y is the return to holders of debt Df of every firm f in state j, where Either Yfj:=

Df for Df � Xfj

(the firm "survived")

Or Yfj:= Xfj

- Cfj for Df > Xfj (the firm is bankrupt).

Z: F x J x R+D x RX x RT[0,1]

� R+Z is the return to the holders of the equities of f in state j, where Either Zfj:= Xfj

(1-Tj) + TjDf - Df for Df � Xfj (the firm "survived")

Or Zfj:= 0 for Df > Xfj

(the firm is bankrupt)

The last three functions have again a different logical role:

B: F x J x R+Y x R+P x R+D x RX x R[0,1]T x R+C

� R+B yields the present market value of the debt Df of firm fS: F x J x R+Z x R+P x R+D x RX x R[0,1]T x R+C

� R+S yields the present market value of the equities of firm fV: F x J x R+S x R+B x R+P x R+D x RX x R[0,1]T x R+C

� R+V yields the present total value of the firm, where Vf: � Sf + BfSince B and S have only their domains and ranges specified, nothing is yet said about how they could be determined from the variables introduced earlier. This is all we do to specify the set DETCp. A thing x is a potential structure of the Kraus and Litzenberger theory, or a potential model iff it satisfies all requirements mentioned thusfar, and hence Bf, Sf and Vf can be, in an x

� DETCp, any nonnegative real number.4 Models: introduction of the axioms on market forces

The set of models of the theory differs from the set of potential models by a specification of how the present market value of debt and equity is determined. This yields a subset DETC

� DETCp of structures:x is a debt equity market system with corporate tax and bankruptcy cost (DETC) iff:

Y (Pj, j � J) have market equilibrium prices Pj (j � J). (An explicit definition of this as a defined function would require extension of DETCp with a set of investors, and functions mapping their probability beliefs on state j � J, risk aversions, time preference and utility functions)1) x is a DETCp

2) P is such that primitive securities in

For convenient notation of the requirements on the functions B and S,

Kraus and Litzenberger (re)number the states j1, j2, .....,jn

in J for every firm in climbing order of the known return Xfj in each state. So

we have, for every f:

Xf1

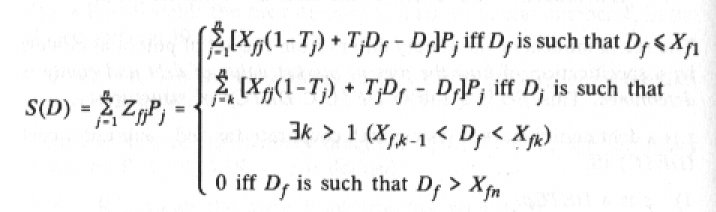

3) B is such that for all firms f

The first of these three functions is meant for the case in which debt Df is such that the firm survives (will not go bankrupt) in every possible state. The second function is meant for the cases where debt is such that the firm is bankrupt in state j = 1,.., k-1 and survives in the remaining states. The third function is meant for the case in which debt is such that in all states the firm will be bankrupt.

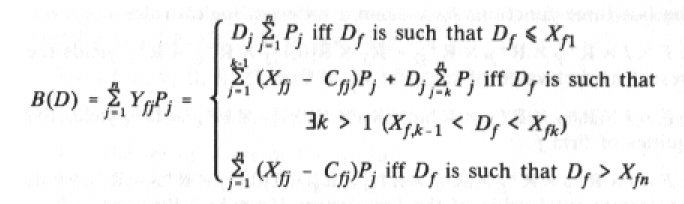

The present market value of debt is thus reduced to the present market value of primitive securities. The same is done for the equity of f:

4) S is such that for all f

The meaning of the tripartition is again bankruptcy in no/some/all possible end-of-period states.

5 Interesting theorems: their exact shape

This ends the list of additional requirements that a structure x

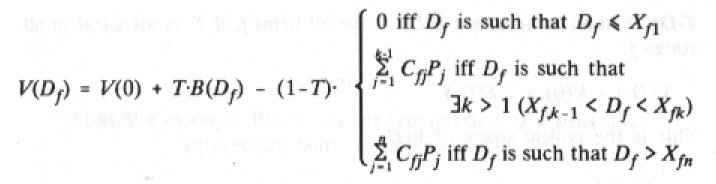

�DETCp must meet in order to be an element of DETC � DETCp. The list is the result of a strategy meant to find the class of structures for which the following theorem T-DETC holds:T-DETC: in all structures x

�DETC, for all firms f, if Tj is identical in all states j (dropping subscript j),

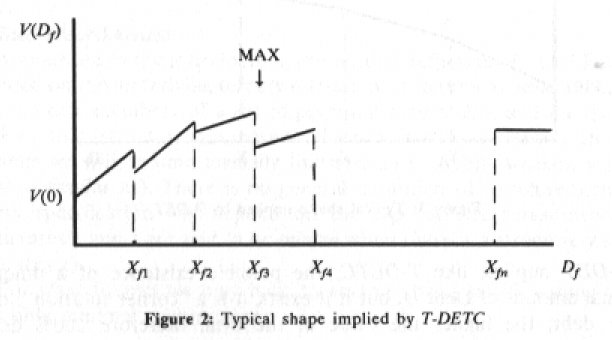

Figure 2 depicts an example of a shape that V(Df) could take for some firm f:

The slopes of the line segments are determined by T and Pj ( Kraus and Litzenberger (1973), p. 916), and every time Df passes the value at which it equals some state's total return of the firm, Xfj, the bankruptcy costs of that state kick down the value of the function V(Df).

T-DETC implies 1) that there can be a unique optimal amount of debt Df, 2) this optimum amount of debt can be "interior", that is, larger than zero and smaller than the total return of the firm in the firm's most lucrative state (Xfn). Figure 2 is drawn as an example of this possibility.

This possibility arises as a result of the introduction of bankruptcy cost in the model. If bankruptcy costs are removed from the structures in DETC and DETCp, a poorer set of structures DET(p), results, where x

�DET(p) is called (potential) debt equity market system with corporate tax. This brings us back to the original paradoxical Modigliani- Miller theorem on the optimal amount of corporate debt in case of the existence of corporate tax; setting Cfj � 0 in T-DETC immediately yields T-DET:T-DET: in all structures x

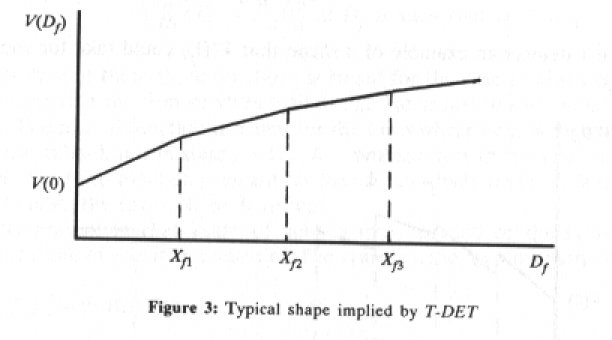

�DET, for all firms f, if Tj is identical in all states j:V(Df) = V(0) + T.B(Df)

This is the typical shape of V(Df):

T-DET implies, like T-DETC, the possible existence of a unique optimal amount of Debt Df but if it exists, it is a "corner solution": the more debt, the higher the value of the firm, therefore 100% debt financing is optimal.

If, finally, tax Tj is removed from the structures, we obtain DE(p), where x

� DE(p) is called a (potential) debt equity market system. This yields the initial Modigliani-Miller Theorem T-DE.T-DE: in all structures x

�DE, for all firms f, V(Df) = V(0)This means that the debt-equity ratio is irrelevant to the value of a firm. The graph becomes a horizontal line.

History would have been nice and simple if Modigliani and Miller had first discovered T-DE in the Kraus and Litzenberger framework presented above, then would have introduced tax to arrive at T-DET, and finally that Kraus and Litzenberger enriched the theory with bankruptcy cost to arrive at T-DETC.

However, Modigliani and Miller did not use the state preference framework. For what this example is meant to illustrate below, we do not need to go into the logical intricacies of reducing Modigliani and Miller's of introducing market forces to the method used by Kraus and Litzenberger.